The Craft Beverage Modernization and Tax Reform Act (CBMA), which follows the U.S. Internal Revenue Code, provides for reduced rates or tax credits for beer, wine, and distilled spirits produced in or imported into the United States.

From 2018 to 2022, U.S. Customs and Border Protection (CBP) has administered the CBMA tax provisions related to imported products. A recent change in the law transferred responsibility for administering the CBMA tax benefits for imported alcohol from CBP to the Alcohol and Tobacco Tax and Trade Bureau (TTB) beginning with products entered for consumption in the United States on or after January 1, 2023. The TTB has announced the following:

- Transition to tax refunds in lieu of reduced entry tax rates and tax credits for imported alcohol. The TTB will now require payment of federal excise taxes at former standard rates at the time of entry on beer, wine, and spirits. Refunds for the difference between the standard rate and the CBMA rate will now be issued upon submission of quarterly requests via a TTB importer portal.

- Foreign producer registration is required. The TTB recently launched the CBMA Foreign Producer Portal on myTTB.gov. Foreign producers are now responsible for registering on the myTTB.gov website and assigning allocations to importers.

- The first refund submission process begins at the end of Q1 2023. Please see next steps below for how to prepare early.

Helpful Additional Foreign Producer Resources:

- TTB’s LIVE Webinar of New CBMA Import Provisions – Dec 14, 2022 04:00 PM in Eastern Time (US and Canada)

- TTB’s CBMA Changes Overview Video

- Schedule a consultation with us

Key Terms:

Please review the key terms below as you prepare to submit your assignment documentation for the 2023 Craft Beverage Modernization and Tax Reform Act (CBMA) tax benefit allocation to MHW.

Manufacturer or Producer

“Manufacturer” and “Producer” are used interchangeably for the purposes of CBMA. A manufacturer or producer is an entity that produces beverage alcohol. For wine, this would be the winery producing the wine. For distilled spirits, this would be the distillery or production facility making the product. For beer, this would be the brewery. In each case, the entity who is the manufacturer or producer for the purposes of CBMA is the one which processes the product into the state (class/type designation) in which it will be tax paid. “Manufacturer” and “Producer” must possess an up-to-date FDA Registration Number in order to qualify.

Importer of Record

CBMA allocations are issued from the producer to the Importer of Record – not the brand owner. Depending upon your relationship with MHW, MHW may act as the importer or record or you may be your own importer of record with MHW handling the logistics and importation. In these two cases, MHW can support with your CBMA processing and management.

TTB Foreign Producer Portal

https://www.ttb.gov/images/pdfs/cbma/Foreign_Producer_System_External_User_Guide_2022-10-25.pdf

This is the training manual where you can find hyperlinks to the sites to register a foreign producer, manage

your registration, authorize additional users, and make assignments of U.S. tax benefits. “Manufacturer” and

“Producer” must possess an up-to-date FDA Registration Number in order to register on the portal.

CBMA Control Group / Foreign Producer Ownership

A Control Group is a collection of manufacturers or producers that share 51% or more ownership. A group

of producers that share 51% ownership (a Control Group) receive a single CBMA allocation. The Control

Group may choose how to manage production and import of products into the US, as well as how it chooses

to allocate the CBMA allocation between its controlled producers, as long as the assignment of CBMA benefit

does not exceed a single allocation. If the individuals or entities that have an ownership interest of 10% or

more in the Foreign Producer also have an ownership interest in other foreign or U.S. distilled spirits

operations, wineries, or breweries using or assigning U.S. tax benefits, you must provide the TTB (via the

portal) information for any individual or entity that owns 10% or more of the foreign producer being

registered. (However, 51% or more ownership is still the requirement to classify a collection of manufacturers

or producers as a control group).

CBMA Allocations

Assigns U.S. tax benefits to U.S. importers by product, tax benefit category, and quantity.

Allocation of Volume

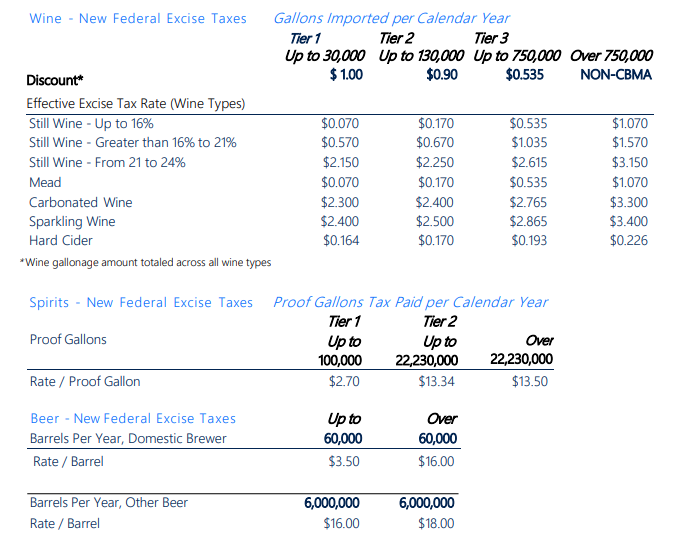

Each control group/producer based on the situation may choose how to allocate wine gallons/proof gallons/barrels to the US importers of record they work with by tax benefit tier. The following tables show the tax rate for each tier of benefit and type of beverage alcohol. The control group/producer indicates the amount of allocation given to the importer in the CBMA Assignment Letter. Each eligible entity (Control Group, if applicable, or independent producer) receives one allocation at each volume tier.