Understanding the Three-Tier System

Learn how MHW will help you navigate the complex regulations of the United States alcohol market to unlock your path to success.

We are proud to partner with the great brands of today and the rising stars of tomorrow.

“MHW has been a trusted and valuable partner to Carolina Wine Brands for more than 10 years. Their operational support, strategic planning, and market entry services have been instrumental to the ongoing growth and success of our portfolio.”

Richard Scelfo Managing Partner, Carolina Wine Brands

“MHW provides the premium level of customer service and reliability demanded of a luxury brand. MHW’s scalability and global services have accompanied our global growth and supported us to independently expand the targeted distribution of our portfolio of prestige cuvées around the world.”

Sebastien Besson CEO, Champagne Armand de Brignac

“MHW has been a fantastic partner and key element in Casa Dragones’ growth and success in the United States. They understand the pace and needs of entrepreneurial ventures, and have provided the support we’ve needed to execute with excellence.”

Bertha González Nieves Co-Founder and CEO, Tequila Casa Dragones

“We have been a partner with MHW since 2014 and have been extremely pleased with their professionalism and deep level of attention to our business and brands. They continue to be a great resource for us and are very responsive to our questions and adaptable to our changing needs. Their entire team has been a key piece to our growth.”

Mike Neises, Vice President and General Manager, Agave Loco and RumChata

“Their best-in-class operations support allows our team to focus on the stories and people that make Combier, Banhez and the rest of our portfolio so unique. MHW was there for case one and every case since, and we couldn’t be happier.”

Curt Goldman, CEO, CNI Brands

“We had a great experience launching Leblon Cachaça with MHW. They were integral to our success, helping us navigate the challenging world of spirits compliance federally and in the various states, and providing a turnkey logistical capability.”

Steve Luttman, Founder and CEO, Leblon Cachaça

120+

Active Markets

33,000+

TTB Colas Filed

80,000+

Current SKUs

$1.6B

Successful Exits

The MHW Difference

Reporting Tools

Discover our proprietary reporting tools to see how MHW will make a difference for your bottom line.

Our People:Teamwork & Integrity

An unparalleled team delivering best-in-class service with transparency and accountability.

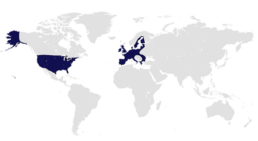

Scope of Services

We are proud to offer our core suite of professional services in the US and EU, with scalable services into more than 100 countries worldwide.

We are proud to be partners with the premier trade associations and service providers of the global beverage industry.